Capital Efficiency Analysis

Executive Summary

As tokenized real-world assets (RWAs) scale toward institutional adoption, liquidity provision for secondary market trading is a central bottleneck. Issuers offering USD-denominated products face a recurring design question: how should they service redemptions? Three broad approaches exist — maintaining a liquidity buffer, seeding DEX liquidity pools per asset, or more recently: deploying a curator-managed instant liquidity vault through Symbiotic’s infrastructure.

This article dives into the design choices comparing capital efficiency differences for an illustrative issuer managing two RWA funds, with a shared $10M USDC liquidity budget. Instant redemptions from Midas’ mHYPER and mF-ONE were used to model the different scenarios and swap flows.

Using scenario analysis grounded in observed redemption data and current DeFi lending yields, the results are stark: an idle buffer (that allocates idle capital to a lending market) can earn up to 6.5%, but reduces the intrinsic APY of the vault strategy or asset. A DEX LP can earn up to 5%, but remains exposed to the risky asset for most of the time and requires double the capital, despite offering weaker liquidity guarantees. Meanwhile, Symbiotic’s instant liquidity product can generate 9%+ without even accounting for additional yield paid by Symbiotic applications on top of it.

Note: this analysis only takes into account 2 assets. With a broader set of assets, the yield gap between Symbiotic’s approach and the idle buffer would likely increase substantially.

The Liquidity Problem in Tokenized RWAs

Most tokenized assets — from private credit to alternative strategies — feature episodic or time-locked primary liquidity: structured redemption windows, T+3 to T+90+ settlement cycles, NAV-based queues, or gated redemptions. An investor wishing to exit before a window reopens or a DeFi protocol needing to liquidate have no natural counterpart. This creates a structural demand for secondary liquidity infrastructure — a mechanism that guarantees an exit at or near NAV at any time.

The market for tokenized RWAs has reached over $30b in asset value as of May 2026, but secondary market depth remains thin for most non-treasury assets. Real liquidity, as Bryan Choe from RWA.xyz notes, "comes from exits, either through a clearly defined redemption mechanism or a deep secondary market with willing buyers". For issuers, how that liquidity is capitalized determines not just the user experience, but the annual cost — or return — on tens of millions in reserved USDC.

Scenario Setup

The analysis models an issuer with two USD-denominated RWA funds and $10M of available capital to build liquidity for those assets. The assets span a range of durations and yields, calibrated using real product data from Midas assets.

| Asset | Proxy | Instant Fee | Redemption Window | Intrinsic APY | Observed Instant Redeem % |

|---|---|---|---|---|---|

| RWA-1 | mHYPER-like | 0.50% | T+3 | 8.00% | 22% |

| RWA-2 | mF-ONE-like | 1.00% | T+35 | 9.50% | 43% |

The proxy data comes from Midas’ frontend and from onchain events emitted by the protocol.

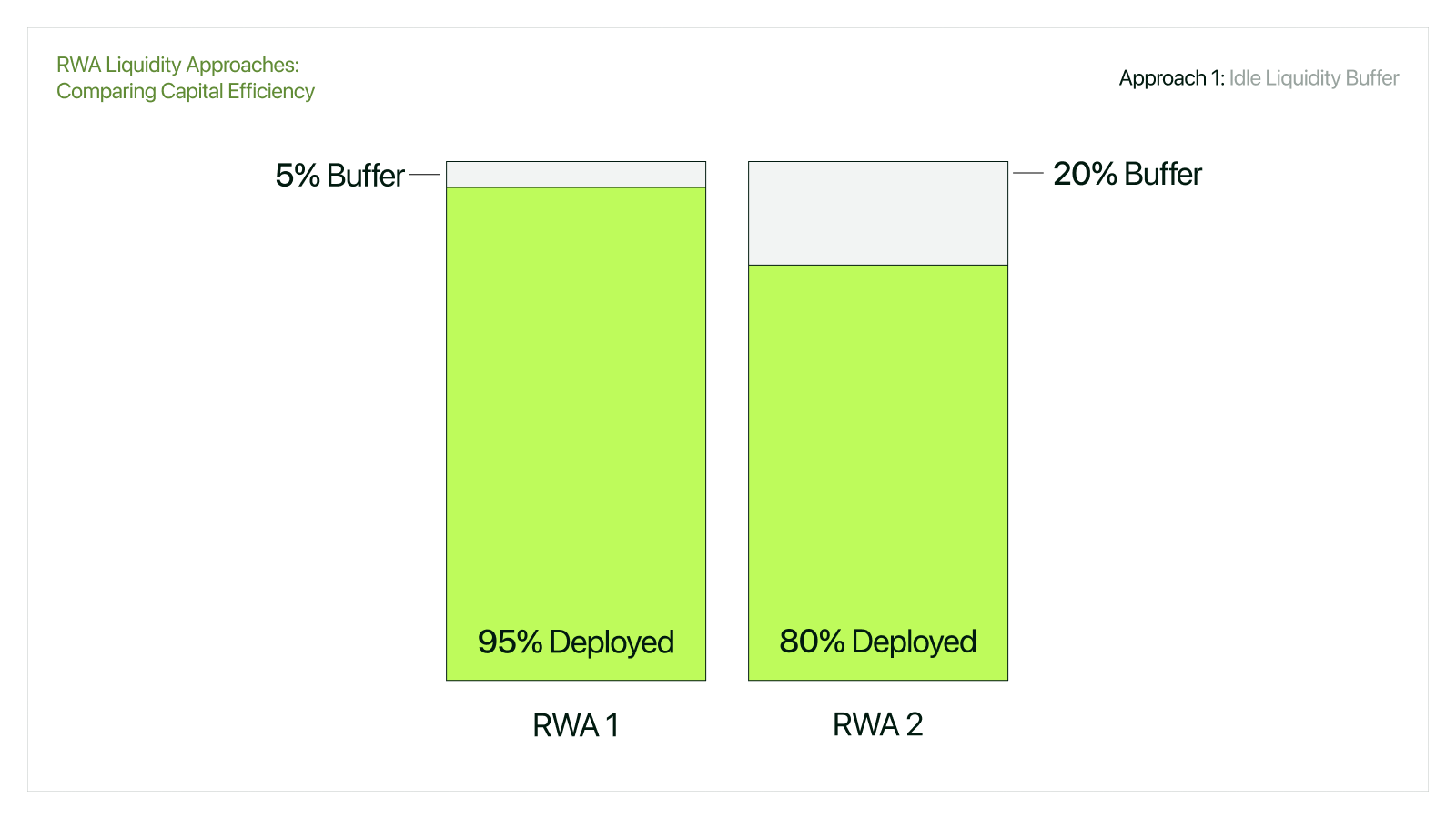

Approach 1: Idle Liquidity Buffer

The simplest approach is a manually managed USDC reserve. The issuer holds $10M in USDC (or short-duration equivalents) earmarked for redemptions. Bots or staff monitor inflows and manually release funds when requests arrive.

Capital efficiency problem: An idle buffer can only allocate capital to highly liquid yield sources, e.g., Morpho, and is almost always embedded into the asset itself. This means the capital cannot be shared across multiple assets. It also reduces the intrinsic APY of the strategy, as part of the capital remains structurally underutilized.

The buffer does provide full coverage flexibility — $5M per asset can, in principle, absorb any single-asset redemption surge. But the capital never works dynamically: it remains limited to highly liquid yield sources and cannot be efficiently shared across assets, reducing overall capital efficiency relative to more productively deployed alternatives.

Outcome on $10M ($5M per asset):

| Income/Cost Item | Amount |

|---|---|

| Base lending yield (4% on idle capital via Morpho) | +$290,000 |

| Redemption spread income | +$361,068 |

| Net annual return | +$651,068 (6.5% APY) |

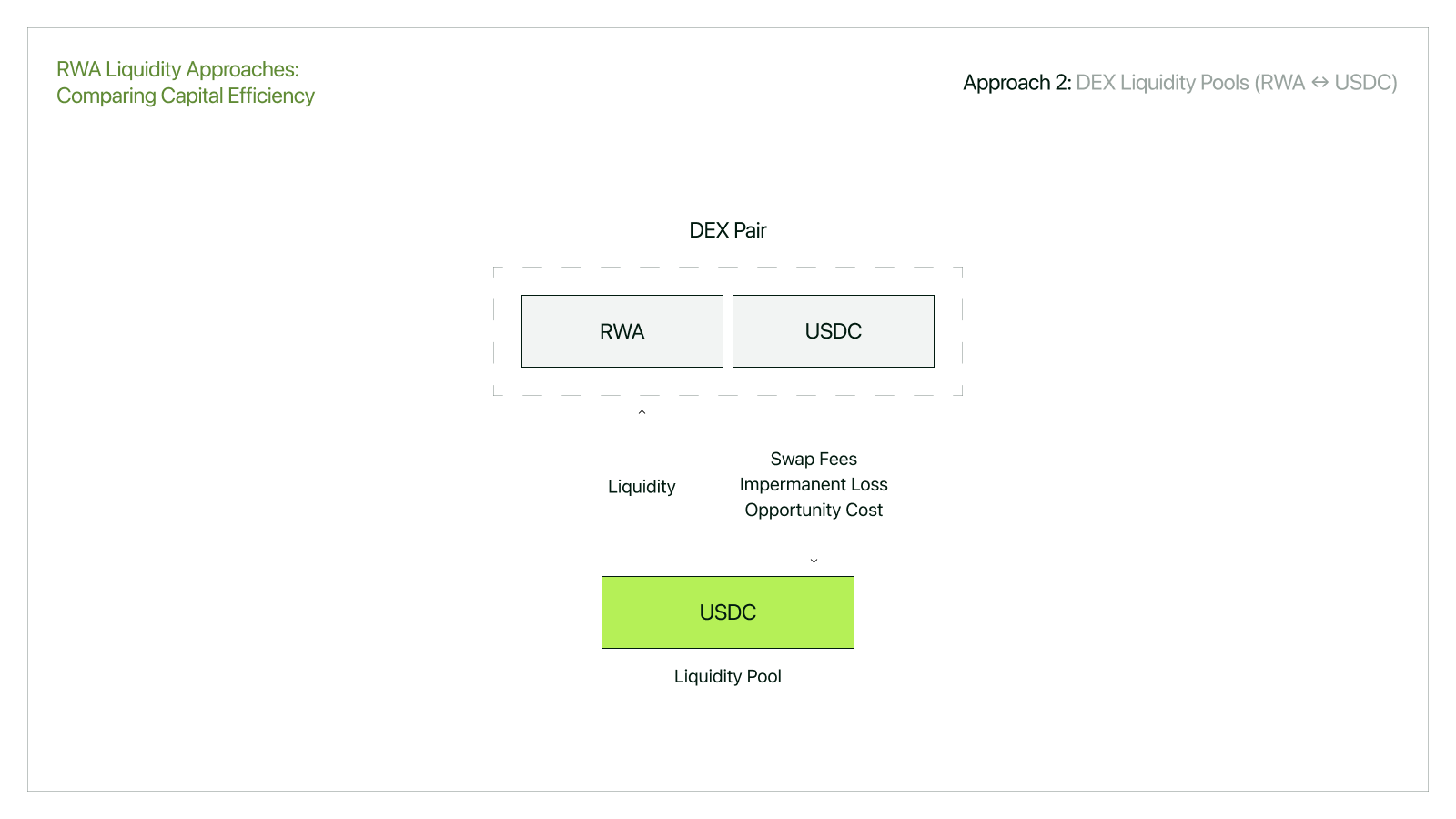

Approach 2: DEX Liquidity Pools (RWA ↔ USDC)

An alternative is to seed secondary market DEX pools — one per asset — so that token holders can swap RWA tokens for USDC at any time. The issuer (or a subsidized LP) deposits $2.5M worth of USDC into each pool, structured as a 50/50 RWA/USDC pair.

However, the structural inefficiencies of this model compound quickly and make liquidity guarantees unreliable at scale.

Siloed Capital

Each pool locks dedicated USDC liquidity per asset. If redemption demand concentrates in one fund — for example, mF-ONE following a macro event — only the liquidity available in that specific pool can absorb exits. Liquidity sitting idle in other pools cannot be dynamically redirected, even if unused. In practice, this fragments capital across asset boundaries despite redemption demand being highly unpredictable.

Continuous Exposure to Underlying Asset Risk

The LP remains exposed to the underlying RWA risk at all times. Half of the capital is directly allocated to the RWA itself, meaning LPs bear the underlying credit, duration, and NAV risk of the asset. Yet despite taking that exposure, the total LP return can still underperform simply holding the RWA directly.

This occurs because the AMM structure continuously sells appreciating RWA exposure back into USDC as arbitrageurs rebalance the pool. The LP captures swap fees, but systematically gives up part of the asset appreciation.

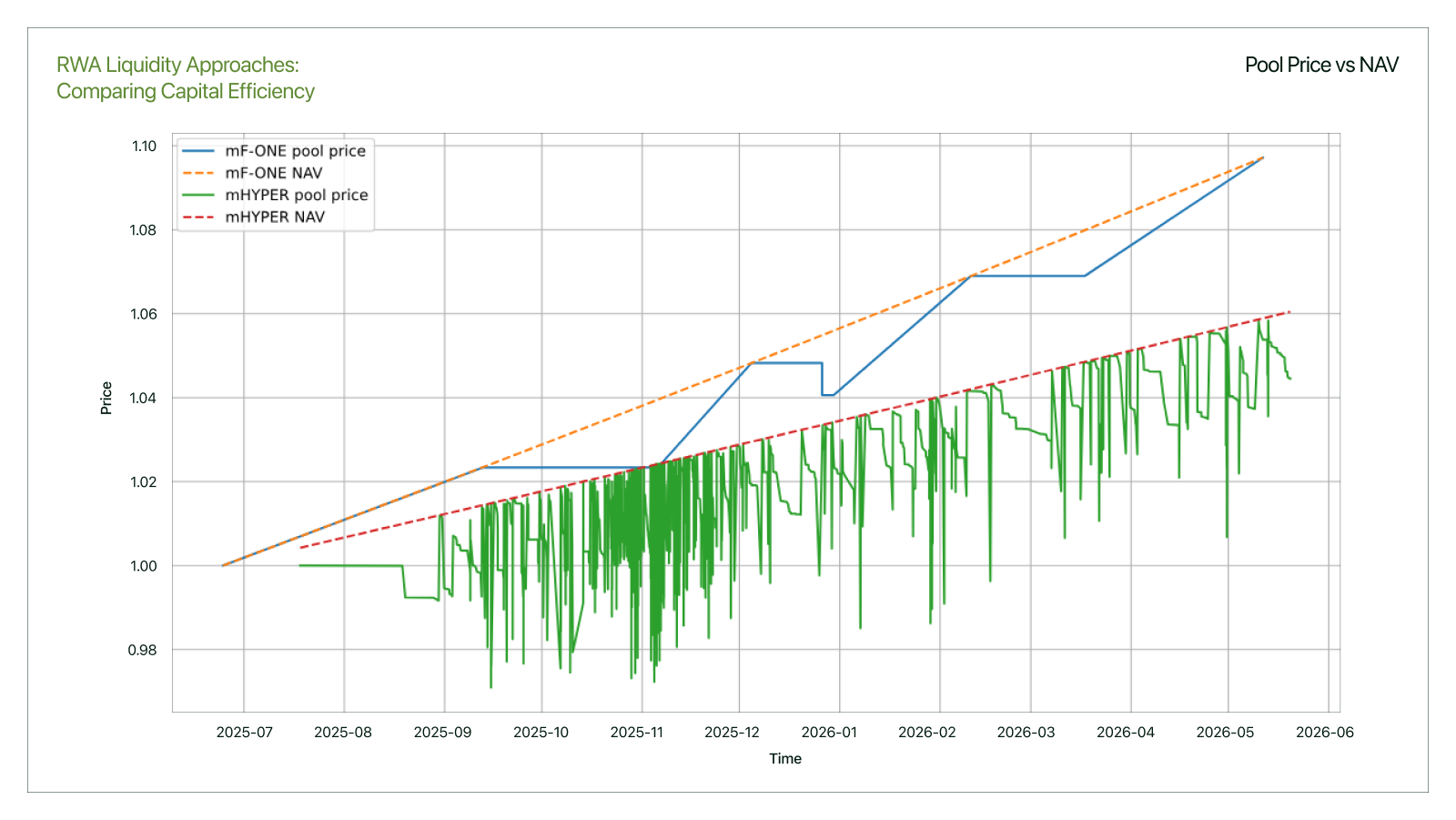

Impermanent Loss from NAV Drift

RWA tokens are yield-bearing instruments whose NAV increases continuously over time. AMMs mechanically rebalance inventory as prices move, which forces LPs to sell portions of the appreciating asset into stablecoins during NAV appreciation.

Our analysis assumes arbitrage opportunities are executed whenever the pool price trades 2% below NAV, while trades stop occurring once slippage exceeds 3%. In practice, this creates a structurally adverse environment for LPs: profitable arbitrage continuously extracts value from the pool during normal NAV appreciation, while stressed redemption periods still fail to guarantee deep liquidity once pool depth deteriorates.

Liquidity Is Still Not Guaranteed

Despite requiring substantial idle capital, DEX liquidity still provides weak guarantees during periods of concentrated exits. Once slippage thresholds are breached, trading activity effectively stops and the pool becomes unusable for meaningful redemptions. In other words, LPs take continuous exposure to the underlying asset while still failing to guarantee reliable liquidity during stress scenarios.

Opportunity Cost

Half of the pool capital remains in USDC rather than fully deployed into the underlying strategy. While this USDC could earn base lending yield on protocols such as Morpho, the return is materially lower than the intrinsic yield of the RWA itself. This creates a direct drag on overall strategy performance.

The result is a structurally inefficient system where LPs absorb underlying RWA risk, impermanent loss, fragmented liquidity, and idle capital costs — while still earning a total APY that can underperform simply holding the underlying asset directly.

Outcome on $10M:

| Income/Cost Item | Amount |

|---|---|

| Swap fee income | +$30,688 |

| RWA Intrinsic APY | +$454,917 |

| Arbitrage fees | +$30,738 |

| Net annual return | $516,343 (5.2% APY) |

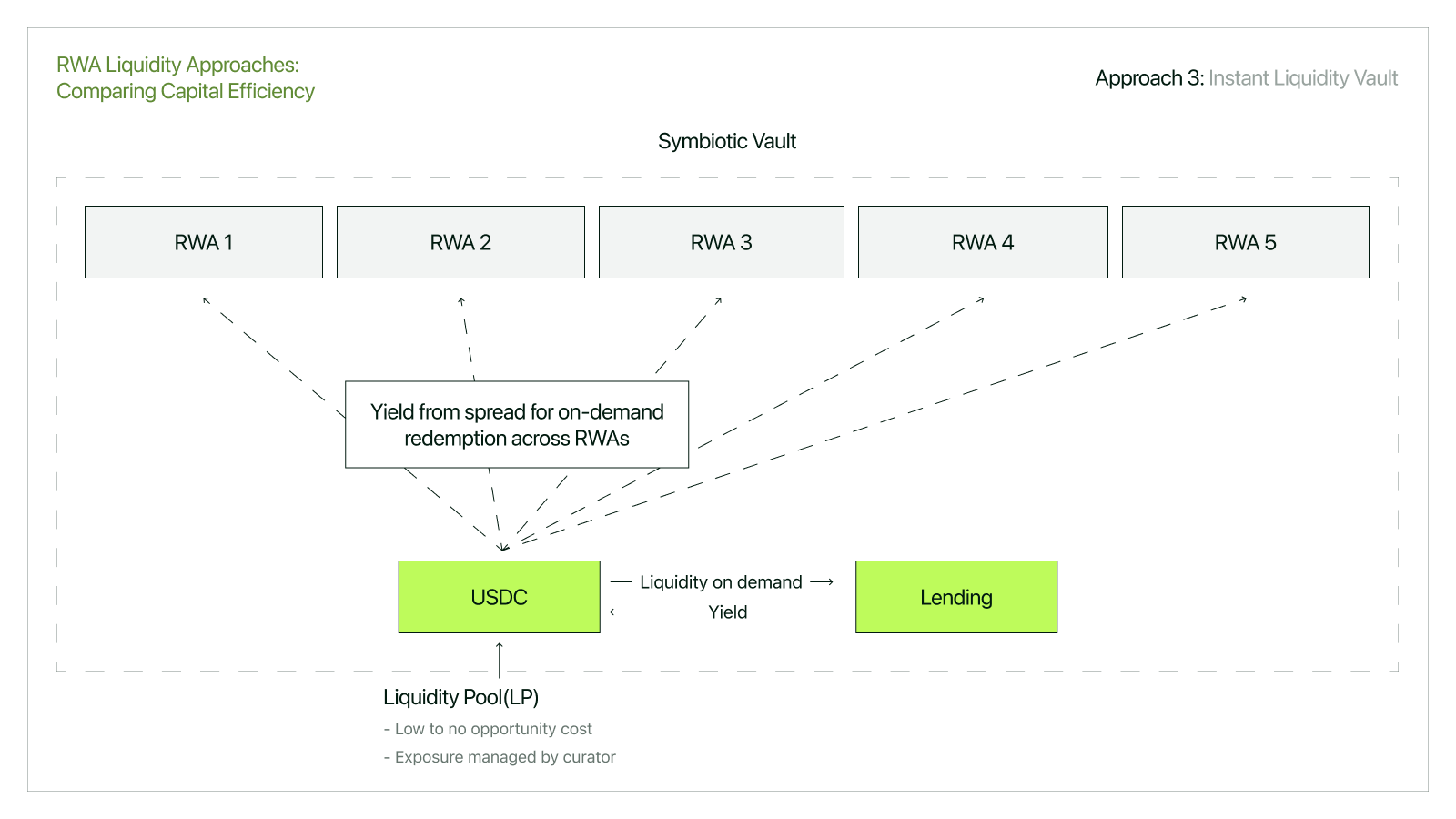

Approach 3: Instant Liquidity Vault

Through Symbiotic’s instant liquidity product, curators can launch USDC vaults to service instant redemptions across multiple RWA assets simultaneously. This vault provides a capital facility to acquire RWA tokens at a discount via an on-chain RFQ (Request for Quote) mechanism or via a fixed discount set per asset by the curator. The acquired RWA tokens are then redeemed at NAV with the underlying issuer during the standard redemption window by the curator — and the spread is shared between them and vault LPs.

How the Vault Works

- A token holder requests an instant exit (through UI/API or aggregators).

- Market makers bid, sign an on-chain order, and the vault receives RWA token at a discount when winning the auction (e.g., 0.5%)

- USDC is drawn by the Symbiotic vault via the Market Maker Symbiotic Contract.

- USDC settles atomically to the token holder.

- The curator redeems the RWA with the issuer at NAV from smart contract custody (e.g. at T+3 or T+35 days) earning the spread minus funding cost.

- Vault LPs receive a share of the spread; idle capital earns base yield via DeFi adapters (e.g. to Morpho).

Capital Efficiency Advantages

Shared pool, dynamic allocation. A single $10M USDC vault covers the two RWA assets. If one asset faces a $5M redemption surge, the vault deploys up to its limit regardless of which asset is in demand — unlike DEX pools where each silo is capped at $2.5M USDC. The curator sets per-asset limits, but the base liquidity is shared.

Earning while idle. The Symbiotic infrastructure routes idle vault capital to DeFi lending adapters (e.g., Morpho) to earn base yield.

Spread income from redemption flows. The vault receives a share of the instant redemption discount.

No impermanent loss. The vault operates via a blind RFQ auction, not as an AMM. There is no constant-product curve continuously rebalancing against NAV appreciation. Capital enters as USDC and exits as USDC (with spread captured), eliminating the structural IL drag that plagues DEX LPs.

Outcome on $10M:

| Income/Cost Item | Amount |

|---|---|

| Base lending yield (4% on idle capital via Morpho) | +$311,641 |

| Redemption spread income | +$401,292 |

| Intrinsic RWA yield while deployed (variable, depending on asset) | +$176,717 |

| Net annual return | +$889,651 (8.9% APY) |

Side-by-Side Comparison

| Metric | Idle Buffer | DEX Pools (4×) | Symbiotic Vault |

|---|---|---|---|

| Available Capital | $10M | $10M | $10M |

| Max single-asset coverage | $5M | $2.5M (USDC side) | $10M |

| Base lending yield | +$290,000 | 0 | +$311,641 |

| Spread / fee income | +$361,068 | +$30,688 | +$401,292 |

| Intrinsic yield on deployed | (reduces intrinsic APY) | +$454,917 | +$176,717 |

| Other yield sources | No | No | Yes (apps & adapters) |

| Net annual return | +$651,068 | +$516,343 | +$889,651 |

| Effective APY | 6.5% | 5.2% | 8.9% |

| Per-asset capital siloing | Yes | Yes (4×) | No |

| Exposure to Risky Asset | Yes | Yes | Minimal |

| Manual ops required | High | Medium | Low |

The vault outperforms the idle buffer by +$239K/year and DEX pools by +$373K/year on the same $10M capital base, while providing stronger liquidity guarantees and maintaining minimal exposure to the risky asset.

Risk Considerations for the Vault Approach

The instant liquidity vault model introduces its own risk profile:

- Duration risk. If an RWA's NAV declines before native redemption completes (e.g., credit event), the vault bears the shortfall between the USDC advanced and NAV recovered. This risk is priced into the fee structure and managed by curator-set per-asset limits.

- Lending adapter liquidity risk. Capital deployed in Morpho may face withdrawal friction during utilization spikes, potentially limiting available liquidity for redemptions.

- Duration mismatch. A vault with a 14-day withdrawal lockup cannot guarantee instant liquidity for vault depositors if it has committed capital to a 35-day redemption cycle (e.g., mF-ONE). Curators must actively manage this mismatch.

- Curator concentration. The model depends on curator-managed parameter-setting and market maker selection. LP exposure to curator quality is material.

These risks are manageable — and are partially compensated by the spread income that prices them. They represent the normal tradeoff of a yield-bearing model vs. the zero-risk, zero-return idle buffer.

The Issuer Perspective

For an RWA issuer, the instant liquidity vault also produces structural benefits beyond the LP P&L:

- Reduced issuer overhead. The vault and curator handle redemption logistics. The issuer doesn’t need to maintain idle capital or directly manage the redemption facility.

- Competitive product differentiation. Offering credible instant redemption is a meaningful distribution advantage. Institutional and semi-institutional investors increasingly require it.

- Scalable across products. A single vault can be authorized to service multiple issuer products simultaneously, with the curator managing per-asset risk parameters — eliminating the need to build separate liquidity infrastructure per fund.

Conclusion

The three approaches reflect three fundamentally different relationships between idle capital and productive yield. The idle buffer treats liquidity as a pure cost center. The DEX approach attempts to generate yield through AMM fees but fails on structural grounds — the economics of AMM LP provision simply do not work for low-volume, yield-bearing, permissioned RWA tokens. The instant liquidity vault turns the same $10M reserve into a productive, multi-asset, dynamically allocated machine: earning base lending yield on idle capital, capturing redemption spreads when deployed, and accruing intrinsic asset yield during the redemption window. For any issuer managing a portfolio of USD-denominated tokenized funds with meaningful redemption demand, the instant liquidity vault is the dominant capital allocation.